- Builders

- Posts

- How to F*ck Up Due Diligence (a true story)

Hey everyone. After a hiatus from my newsletter, I’m back to send out my thoughts on acquiring and operating SMBs. If you’re receiving this email, it means you signed up for my email list, most likely via my X account @chrisxmunn. I’m planning to send a new edition every week from now on. Thanks for reading!

I’m hosting workshop on Building a Killer Sales Team on June 13th. It’s free and will be jam packed with free resources on how to build and manage a sales team.

Would love to see you attend. Did I mention it’s free?

I f*cked up due diligence on my first acquisition.

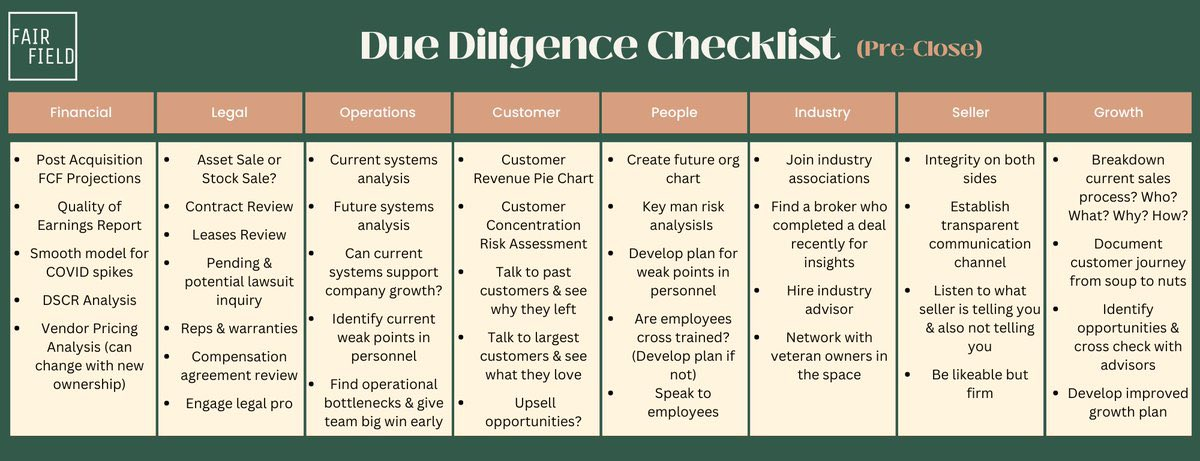

**I’ve included my diligence checklist at the end of this email to help you avoid my fate**

In February 2020 (perfect time to buy a business, right?) I was buying a mom & pop contracting business.

I had just come out of a career doing financial due diligence, so I assumed analyzing this deal would be a piece of cake. The deal was much smaller and less complicated than the huge deals I worked on for clients at my old job. I figured that I was smart enough to immediately identify any red flags.

While I knew how to dig into the financials and conduct DD on the financial side, I knew very little about the operations side. This would come back to haunt me.

During my due diligence, the husband and wife team were very responsive and had their stuff together. I received everything I asked for pretty quickly - which is not the norm these SMB deals. However, for about 5% of the questions I asked, I’d get a weirdly muddled answer that didn’t quite make sense.

Most of these questions with odd answers had to do with the client base. I was told the business had about 30 clients. But my digging into the financials supported that supposed fact, so I didn’t question it.

The sellers’ odd responses weren’t necessarily a red flag. More like a yellow flag.

Some people are just bad at explaining certain things or don’t fully understand how to explain some aspects of their business. Nothing wrong with that, I thought.

Well, it was my mistake to not drill down into those odd answers more.

Just after closing day, I realized my mistake.

The seller tells me that the majority of the contracts are actually through a contractor and we are simply subcontractors. A LARGE percentage of the contracts.

It was clear the seller went through great lengths to hide this. I would have paid substantially less for the business had I known the true nature of those contracts - and the seller knew it!

Instead of 30 clients, we actually had more like 6. And I thought the business DIDN’T have a customer concentration risk.

We immediately started losing business with the contractor, and demand for our service collapsed in March of 2020. It looked like we’d made a massive mistake in buying this business only a few weeks after closing.

Luckily, the damage wasn’t horrible in the end. The seller note (loan given to the buyer by the seller) actually got forgiven because the seller lied, and we dodged a bullet financially.

Luckily, this ended up being a somewhat costly learning experience, and not a fatal blow to our new venture.

What did I learn about due diligence?

The first thing I learned was to drill down on yellow flags.

Many amateur business buyers assume that red flags will slap them in the face.

But this is almost never the case due to Information asymmetry.

The seller will ALWAYS have more information than you. If they want to mislead you, it will actually be easy for them to do so. They have years of experience with the business, while you only have a few weeks of background information.

If the seller wants to hide some skeletons, they’ll know exactly where to hide them.

This is why you must drill down on the yellow flags.

If an answer to a question doesn’t quite make sense, drill down further. Either you’ll resolve your initial confusion by getting more information, or you’ll realize that there’s a problem.

I’ll let you decide if you walk away from a deal when you catch the seller in a lie. There are basically two schools of thought, highlighted by the two tweets below:

Walk away from any deal the second you catch a seller in a lie.

Almost all sellers lie/exaggerate about something. If you walk away everytime, you may never buy a business! Just make sure you understand the nature of the dishonesty and give yourself a margin of error.

https://x.com/moseskagan/status/1780281136737816615 (this one is about real estate specifically, but also applies to SMBs in my opinion)

After his harrowing learning experience, here’s the Due Diligence Checklist I have put together over the last few years of acquiring SMBs.

I want to clarify an important distinction about due diligence:

The point of the exercise is NOT to obtain perfect items in every category from the seller. You can’t just walk away the second you notice some 2% discrepancy between the proforma financials and the QoE report.

Every deal will have some sort of hair. The point is to gather enough information about each of the above areas to feel comfortable with (1) the amount of money you’re offering for the business and (2) operating the business.

Yes, there will be errors, omissions, and mistakes on the seller’s end for many of these items.

The point is to understand exactly what you’re buying as much as possible, not to grade the seller like a high school English teacher looking for a perfect score.

For some reason, we expect SMB owners to be perfectly organized and on top of absolutely everything on this list. But if the seller of a $2 million contracting business was that organized and skilled at operations to have all their ducks in a row, the company would probably be much larger than $2mil.

If you want my due diligence checklist on Notion, feel free to download it here.

Thanks for reading!

-Chris